How Insurer-Pharmacy Negotiations Set Generic Drug Prices

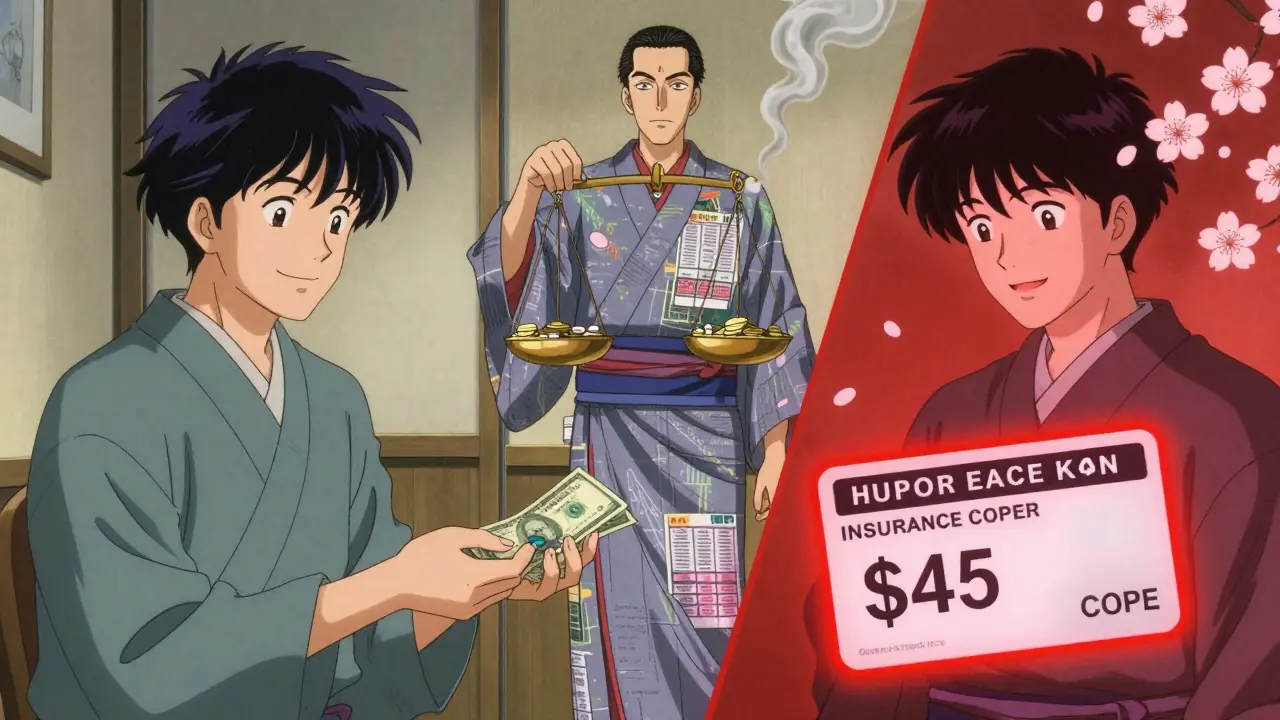

When you fill a prescription for a generic drug like metformin or lisinopril, you might expect to pay a few dollars. But sometimes, your insurance copay is $45 - while the cash price at the pharmacy is just $4. This isn’t a mistake. It’s how the system works.

Who Really Sets the Price?

You might think your insurer or pharmacy sets the price for your generic medication. But in reality, it’s mostly Pharmacy Benefit Managers - or PBMs. These are middlemen hired by health plans to manage drug benefits. Think of them as the invisible negotiators behind your prescription receipt. Three companies - OptumRx, CVS Caremark, and Express Scripts - control about 80% of the U.S. market. They don’t sell drugs. They don’t dispense them. But they decide how much pharmacies get paid and how much you pay at the counter.The MAC List: What You’re Not Seeing

PBMs create something called a Maximum Allowable Cost (MAC) list. This is a secret spreadsheet that says the highest amount they’ll reimburse a pharmacy for a generic drug. It’s not based on what the drug actually costs to make or buy. It’s based on outdated formulas like Average Wholesale Price (AWP) or National Average Drug Acquisition Cost (NADAC), which don’t reflect today’s market. A pharmacy might pay $1.20 for a 30-day supply of generic omeprazole, but the PBM’s MAC might be $3.50. Sounds fair, right? Not quite.Spread Pricing: The Hidden Profit

Here’s where it gets tricky. PBMs charge your insurance plan $12 for that same $1.20 drug. Then they pay the pharmacy $3.50. The $8.50 difference? That’s spread pricing. It’s pure profit for the PBM - hidden from you, your doctor, and often your insurer. This isn’t rare. Evaluate Pharma estimated in 2024 that spread pricing generated $15.2 billion in undisclosed revenue last year, with two-thirds of it coming from generic drugs. That’s money pulled from your plan’s budget, not your pocket - but it’s still money that drives up premiums and plan costs over time.

Why Your Copay Is Higher Than Cash

You’ve probably heard, “Use your insurance - it’s cheaper.” But for generics, that’s often not true. Because PBMs set your copay based on their inflated MAC price, not the real cost. If your plan has a $45 copay for a drug the pharmacy bought for $1.20, you’re paying $45 - even if you could walk out with it for $4 using GoodRx. And here’s the kicker: pharmacists are often legally blocked from telling you. Gag clauses in PBM contracts prevent them from saying, “Hey, cash is cheaper.” In 2024, the CMS reported 92% of PBM contracts still contain these clauses. That’s not a loophole. It’s a rule.Clawbacks and Broken Trust

Even after you pay your copay, the pharmacy might still get hit. PBMs do something called clawbacks. After processing your claim, they look back and say, “Oh, we overpaid.” Then they take money back from the pharmacy - sometimes weeks later. A 2023 FTC report found 63% of independent pharmacies have been clawed back at least once. For a small pharmacy, losing $20 on a $5 generic can mean the difference between staying open and shutting down. Between 2018 and 2023, over 11,300 independent pharmacies closed - many because PBM reimbursement rates dropped below their actual costs.How Pharmacists Are Forced to Play the Game

Running a pharmacy today isn’t just about filling prescriptions. It’s about decoding PBM contracts. Pharmacists spend 200-300 hours a year just trying to understand reimbursement rules that change without notice. Many have to run two pricing systems: one for insurance, one for cash. They need specialized software that costs $12,500 just to start. And if they get it wrong, they’re penalized. One pharmacist in Ohio told a reporter, “I have to check three different apps before I can tell a patient how much they’ll pay. It’s not healthcare. It’s accounting warfare.”

Cassie Widders

January 13, 2026 AT 01:14So you're telling me I paid $45 for metformin while my neighbor paid $4 cash? And the pharmacist couldn't even tell me? This isn't healthcare. It's a rigged game.

Windie Wilson

January 13, 2026 AT 19:08Let me get this straight - the same drug costs $1.20, your insurance pays $12, you pay $45, and the pharmacy gets $3.50? And we call this capitalism? 😂

Daniel Pate

January 14, 2026 AT 21:07This system isn't broken - it's working exactly as designed. PBMs aren't intermediaries; they're rent-seekers. They profit from opacity, and the entire structure incentivizes complexity over care. We're not just overpaying - we're subsidizing corporate inefficiency disguised as administration.

The MAC lists are archaic. The clawbacks are predatory. The gag clauses are unethical. And yet we keep calling it a market. No market functions this way without regulation - and even then, the regulation is toothless.

The real tragedy? The people who suffer most aren't the ones with insurance. It's the independent pharmacists trying to survive on reimbursement rates lower than their rent. When your profit margin is less than the cost of a coffee, you're not running a pharmacy - you're running a charity.

Amanda Eichstaedt

January 16, 2026 AT 04:57I used to think insurance was helping me. Then I started using GoodRx. Now I pay $3 for my blood pressure med and laugh at my coworkers who still pay $40. It's not about loyalty - it's about survival. If the system won't help you, you have to help yourself.

Also, why do we still let PBMs exist? They don't add value. They just move money around like magicians with a bad sleight of hand. The only thing they're good at is hiding the ball.

Alex Fortwengler

January 16, 2026 AT 06:48Big Pharma + PBMs + insurers = the ultimate cartel. This is how they control you. They want you confused, dependent, and too tired to fight. The government knows. They just don't care. You think Biden's executive order matters? It's a PR stunt. The real players own both parties. Wake up.

jordan shiyangeni

January 17, 2026 AT 01:48It's not merely unethical - it's a violation of the fiduciary duty owed to patients. When third-party entities profit from the deliberate obfuscation of drug pricing, they are engaging in a form of economic fraud. The MAC list is not a pricing mechanism - it is a legal fiction engineered to extract surplus value from vulnerable populations. The gag clauses are not contractual terms - they are violations of informed consent.

Pharmacists are not merely employees - they are moral agents trapped in a system designed to silence them. Their professional integrity is being systematically eroded by corporate mandates that prioritize profit over patient welfare. This is not capitalism. This is corporatized medical feudalism.

And yet, we continue to treat this as a policy debate rather than a moral emergency. We must demand accountability. We must sue. We must boycott. We must replace these institutions entirely.

Monica Puglia

January 18, 2026 AT 00:42PSA: Always ask for the cash price 🙏 I didn't know this until last year - now I save $80/month on my meds. Also, if your pharmacist looks guilty when you ask about GoodRx... that's not your fault. It's theirs. And it's wrong.

❤️ to all the small pharmacies fighting this. You're the real heroes.

Lelia Battle

January 18, 2026 AT 18:04The deeper issue here is the erosion of trust in institutions we're told we can rely on. We assume our insurers are working in our interest, but they've outsourced their moral responsibility to entities with no accountability. The PBM model doesn't just distort pricing - it distorts the entire relationship between patient, provider, and payer. It turns healthcare into a transactional puzzle rather than a covenant of care.

And yet, we keep playing along. We blame pharmacies. We blame doctors. We blame our premiums. But the real architect of this system is the illusion of choice - the belief that we have agency when, in fact, the rules are written by those who profit from our confusion.

Transparency laws are a start. But what we need is a redefinition of value: not what's cheapest to pay out, but what's healthiest to deliver.

Ben Kono

January 20, 2026 AT 09:43So why don't we just ban PBMs already I mean like come on this is ridiculous

Jose Mecanico

January 22, 2026 AT 07:31I’ve been a pharmacy tech for 12 years. This is real. We get paid less than the cost of the bottle sometimes. And we’re told to smile while we do it. No one talks about the burnout. No one talks about the pharmacists quitting because they can’t afford to keep working here.

Eileen Reilly

January 23, 2026 AT 02:53ok but like… why are we still surprised? the whole system is designed to extract money from sick people. its not a bug its a feature. also goodrx is a scam too they take a cut too dont be fooled

Darryl Perry

January 23, 2026 AT 20:02The math doesn't lie. $1.20 cost, $45 copay, $8.50 spread. That's not capitalism. That's theft with a W-2.

Abner San Diego

January 24, 2026 AT 01:55They closed 11k pharmacies? And we’re still letting PBMs run wild? This isn’t healthcare. This is colonialism with a white coat. America’s drug pricing is a global embarrassment. We pay more than every developed nation and get worse outcomes. Shameful.

Rinky Tandon

January 25, 2026 AT 16:34Let me explain this in terms you can comprehend - PBMs are the financial parasites of the American healthcare ecosystem. They exploit the structural ignorance of the populace and the regulatory inertia of the state. Their MAC lists are not pricing tools - they are instruments of economic subjugation. The clawbacks are not accounting adjustments - they are predatory financial strikes against small businesses. The gag clauses are not contractual provisions - they are violations of the Hippocratic Oath by proxy. The entire PBM architecture is a manifestation of neoliberal decay - a cancerous growth on the body of public health. Until we dismantle these entities and replace them with publicly accountable entities, we are not healing - we are being looted.

Konika Choudhury

January 27, 2026 AT 06:42Why are we even talking about this like its new? In India we have generic drugs at 10% of the price and no one is confused. This is what happens when you let corporations run healthcare. America needs to wake up

Amanda Eichstaedt

January 28, 2026 AT 09:54Actually I just called my local CVS and asked for the cash price - it was $2.99. My copay was $42. I paid cash. The pharmacist looked at me like I was a genius. Then whispered: 'Thank you.' I didn't even know I was supposed to feel guilty for doing the smart thing.